By: Jianyu (Fisher) Shi

strategic business development; Udacity self-driving car alumni;

China will be one of, if not the biggest market for self-driving cars.

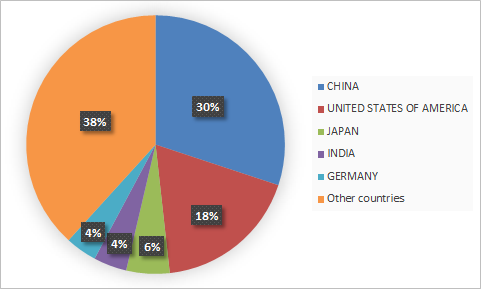

In 2017, 29 million new vehicles were sold in China, more than US, Japan, and India combined. The number of new vehicles sold will reach 37 million by 2025 assuming a 3% annual growth rate (3% is a conservative estimate as the CAGR in the past 5 years is 8.57%).

How many of those 37 million cars will have self-driving functions? According to a plan for automotive industry (link in Chinese) published by Chinese government last year, 25% of new vehicles will be Level-2 or Level-3 autonomous vehicles by 2025 (all the levels mentioned in this post are SAE standard). Level-4 and Level-5 autonomous vehicles will start to enter the market.

The huge market potential attracts more and more companies to enter the self-driving car industry. Tech giants, startups, and OEMs in China all want to play a crucial role in the self-driving car era. Let’s take a look at who they are, and how they are doing right now.

Tech giants

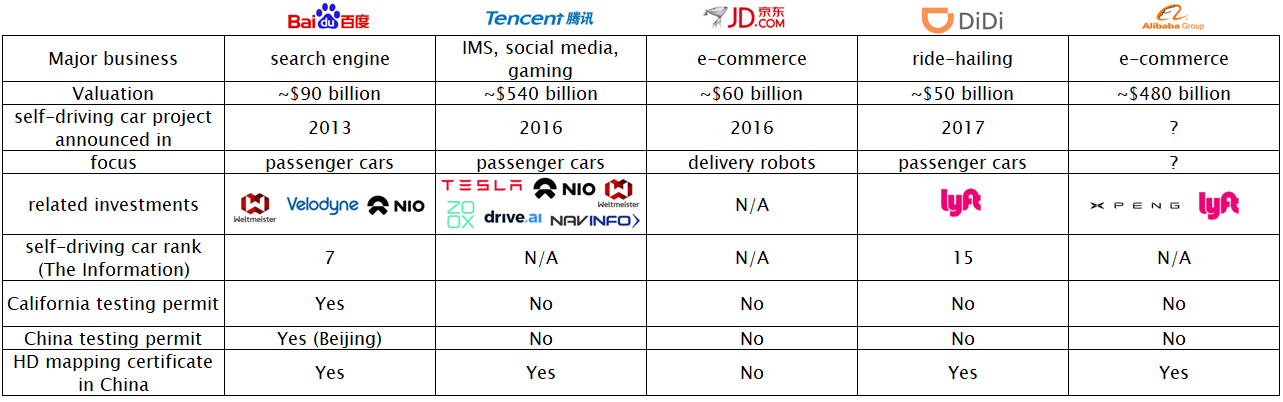

Baidu, Didi, Tencent, and JD all announced their self-driving car projects. Although not officially confirmed yet, it is widely believed that Alibaba is also developing autonomous vehicles, most likely for its warehouses and delivery services.

Other than the resources and engineering talents, the control over HD mapping business is another important advantage of tech giants. Baidu and Alibaba own two of the 3 major HD mapping companies in China, and Tencent is the 2nd-biggest shareholder of the third company.

Baidu is widely considered the leader of the self-driving car in China.

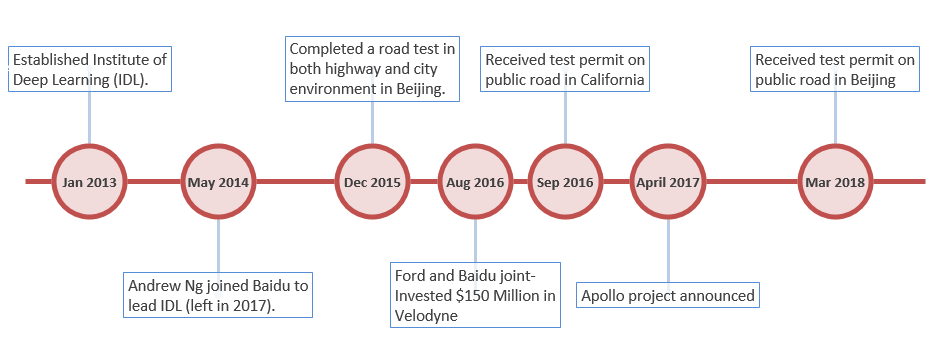

Baidu started developing self-driving car in 2013, when few Chinese companies showed real interest in this field. Currently it’s testing its self-driving cars in both Beijing and California, with a goal to achieve autonomous driving on highway and certain city roads by end of 2020.

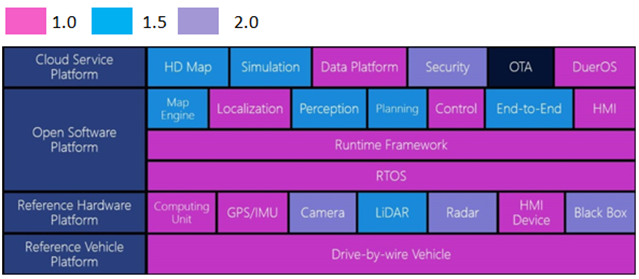

In April 2017, Baidu announced Apollo, an open-source platform for self-driving cars. The ambition of the Apollo platform is to build an ecosystem for OEMs, startups, suppliers, and research facilities to integrate resources and share data.

The list of Apollo participants keeps growing. Within a year, more than 80 partners have joined Apollo platform.

In March 2018, Baidu became the first company receiving permit for testing self-driving cars on public roads in Beijing.

The other tech giants are late to the game, but they are catching up fast.

Didi announced its self-driving car project In 2017. Within a year, it obtained the certificate for HD mapping in China. In February 2018, Didi started testing its self-driving fleet in 3 cities in both US and China.

In 2016, Tencent established its self-driving car lab in Beijing to develop Level 4/Level 5 self-driving technology. Tencent is aggressively hiring engineers for its self-driving car lab with a goal to grow the number of engineers from 50 to 150 in 2018. Its test vehicle was recently spot on the public road in Beijing.

As an e-commerce company, JD’s is interested in self-driving delivery robots. Since 2016, JD has been developing low-speed delivery robots with the help of IDRIVERPLUS, a Chinese self-driving car startup. In June 2017, JD showcased its delivery robot in an University in Beijing.

startups

Chinese Self-driving car startups fall into these 5 fields: full-stack solution, AI chips, LiDAR, computer vision, and Electric Vehicle.

Full-stack solution

Startups working on full-stack solutions can be divided into 2 groups: those who focus on passenger vehicles, and those who focus on commercial vehicles.

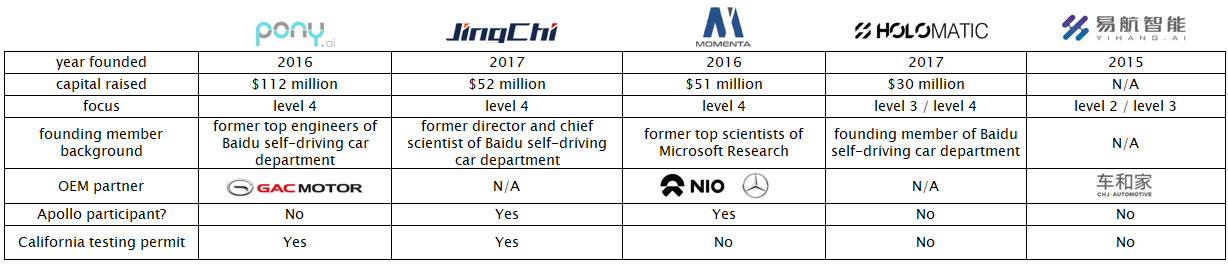

Although companies in the passenger market are very young (most of them are were just founded in the past 2 years), they’ve raised enormous amount of money and some of them already formed partnerships with OEMs. Similar to to Google/Waymo, Baidu also has challenges to keep its top talents. Pony.ai, Jingchi, and Holomatic were all founded by former Baidu employees.

Although commercial market is not as “sexy” as the passenger market (just look at the capital raised by these two groups), the first successful self-driving car company will probably come from commercial market. There’s clear economic value in deploying self-driving vehicles to reduce costs for drivers, and it is much easier to build self-driving vehicles in a controlled environment than building a self-driving taxi fleet. Road sweeper and trucks in ports are likely to be the first two verticals to utilize self-driving technology in China.

AI Chip

Horizon robotics and Cambricon are two well-funded (both raised $100 million) AI chip startups in China.

Kai Yu, founder of Baidu Institute of Deep Learning, left Baidu in 2015 and founded Horizon robotics to develop embedded computer vision processor for video surveillance and self-driving cars. 2 years later, Horizon announced Journey, its first computer vision chip for self-driving cars. Journey is capable of recognizing up to 200 objects such as pedestrians, vehicles, non-motor vehicle, lane lines, traffic lights, etc. at 30 fps for 1080p videos.

Cambricon is developing more general-purpose AI chips,which can be used in typical AI applications such as computer vision, voice recognition, and natural language processing. The company is also developing a chip for self-driving cars, but did not announce when the product will be available to the market.

One major challenge for both of these two companies is to make automotive-grade chips.

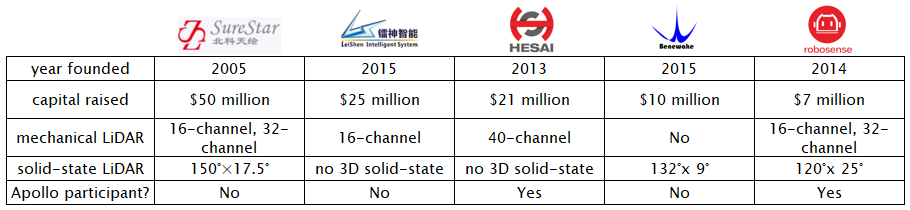

LiDAR

All LiDAR startups have one question to answer: How do they compete with Velodyne, the dominating player in the self-driving car LiDAR market with more than 95% of the market share and a newly-built factory that is capable of producing 1 million LiDAR/year? Luckily for Chinese startups, there are still chances. As the Demand for LiDAR in China is currently low, Chinese startups still have time to develop next-generation products and scale up production.

Computer Vision

With the recent advancement in deep learning, a lot of computer vision startups emerged between 2013 and 2015. Many of those startups want to be the “Mobileye in China”, but most of them struggle to close deals with OEMs. SenseTime is one exception. As an AI unicorn, SenseTime formed a partnership with Honda to develop self-driving cars together. Another exception is MINIEYE, which is working with Xpeng, a Chinese electric vehicle startup.

Electric Vehicle

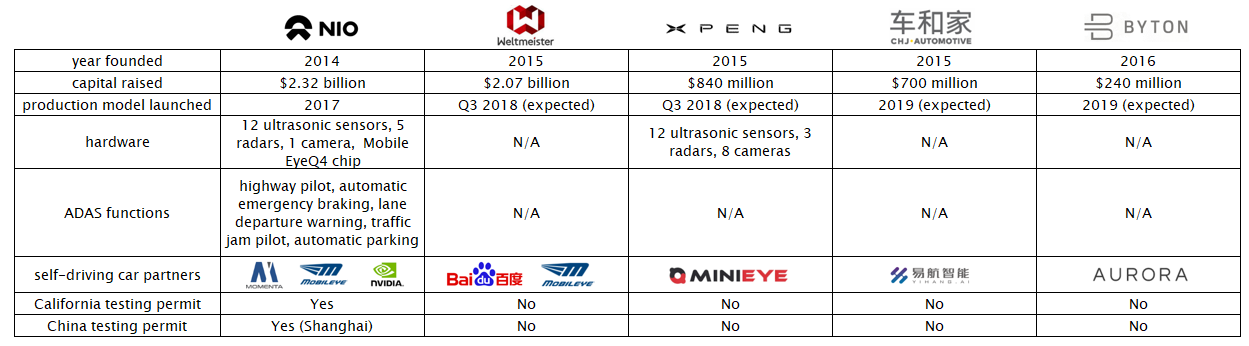

Chinese EV startups all consider self-driving technology as the key to their future success. However, as they all face tremendous pressure to launch their cars to the market as quickly as possible, none of them can afford to wait for level-4 technology to be ready. Just like traditional OEMs, EV startups choose to start with level-2 instead of directly developing level-4 cars. In December 2017, NIO launched ES8, the first car in China with level-2 self-driving functions. It is worth mentioning that ES8 is equipped with Mobileye EyeQ4chip, which makes it possible to upgrade the car to level-3 with an OTA upgrade.

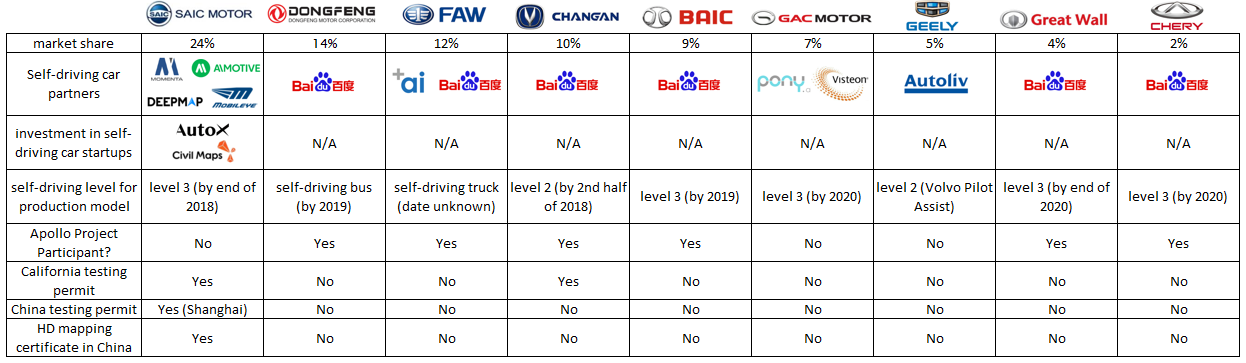

OEMs

As the biggest OEM in China, SAIC Motor is working closely with its technology partners to make sure it will keep its leading position in the era of self-driving cars. The company plans to be the first company launching level-3 car in China by the end of 2018.

Other OEMs are working hard to keep up. Participating in the Apollo project is a popular choice among OEMs to jump-start their self-driving car development, except for GAC Motor and Geely (the company acquired Volvoin 2010). GAC decided to work with the top-notch engineers at Pony.ai. Geely chose to work with Autoliv. In April 2017, Autoliv and Volvo formed a joint venture called Zenuity to develop self-driving cars together.